Remaining Top of Wallet in the Digital Age

Friday April 4, 2025 | Marcus Rothaar, Data Analytics Development and Delivery

The rise of digital payments has transformed consumer behavior, and financial institutions must adapt to remain competitive. Mobile payment adoption is now mainstream, with 74% of consumers using their phone’s payment app, according to a recent Raddon Research Insights survey of more than 1,500 consumers nationwide. However, the competition to be the primary card in these apps is fierce. Nearly 9 out of 10 mobile-payment users default to just one card within their mobile-payment ecosystem. This means that if a financial institution’s card isn’t selected as the primary option, the institution risks being left out entirely.

The shift to mobile payments is especially pronounced among younger consumers, with 97% of Gen Z and 93% of Millennials having a card loaded onto their smartphone’s payment app. As shown in the chart below, even Gen X (80%), baby boomers (51%) and traditionalists (28%) are increasingly adopting mobile payments. As mobile wallets become the center of financial transactions and payments, card issuers must implement strategies to secure top-of-wallet status within digital payment ecosystems.

Figure 1: Percent of consumers with any card loaded on mobile device

Having at least one card in a digital wallet is nearly ubiquitous among Gen Z

Source: Delivery and Payments, Raddon Research Insights, 2024

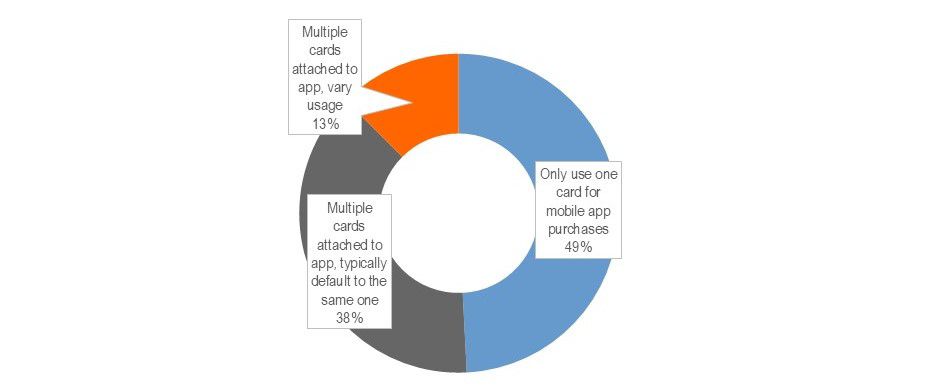

While 67% of mobile-payment users load their primary credit card and 55% load their debit card from their primary financial institution, there is still a significant portion that also add other credit cards (21%) and other debit cards (24%). Additionally, loyalty and store-branded cards compete for space in mobile wallets. But even among consumers who load multiple cards to the phone’s payment app, they typically default to using the same card. As shown in the chart below, only 13% of mobile-payment users who have multiple cards attached to their phone’s payment app tend to rotate cards when making purchases.

Figure 2: Cards used for mobile payments

Nearly 4 in ten have multiple cards in their digital wallet, but tend to gravitate toward the same one

Source: Delivery and Payments, Raddon Research Insights, 2024

Given this landscape, card issuers need to focus on both incentives and engagement to ensure their card remains the go-to option.

Strategies to secure primary card status

1. Competitive rewards

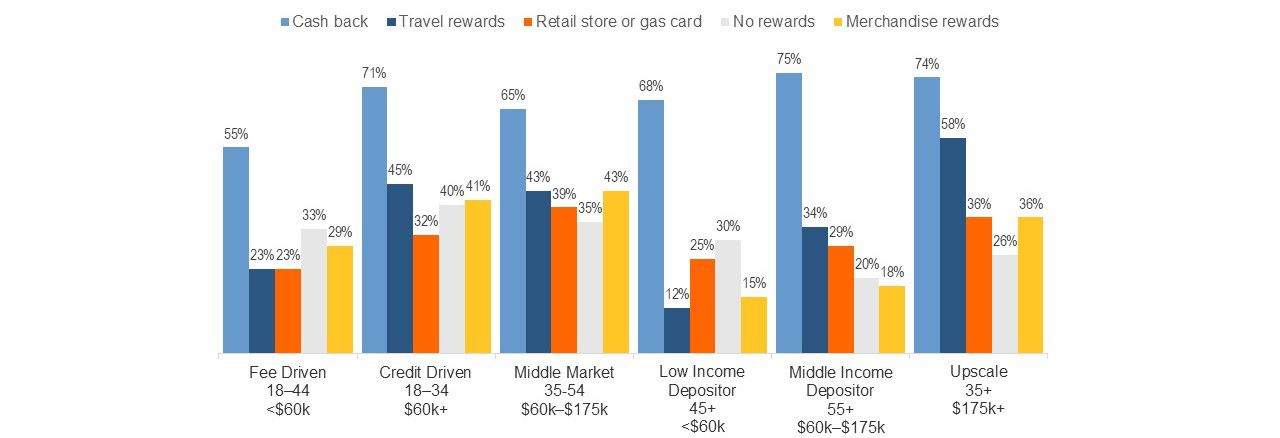

Evaluate your card portfolio to ensure reward programs are competitive and marketed effectively. Raddon research shows that card rewards continue to be top of mind for consumers, with rewards cited as the top feature by cardholders describing their primary or most used card. But not all cardholders are alike, and each may value different types of reward programs. This variety is highlighted by the Raddon consumer segment differences shown in the chart below, which segments consumers based on their age and household income. An example of these differences is the increased importance that an Upscale household places on travel reward programs compared to other segments, particularly the Low-Income Depositor segment.

Figure 3: Type of credit cards used by consumers, by household age and income

Different credit card features are going to stand out to different consumers

Source: Delivery and Payments, Raddon Research Insights, 2024

2. Personalized marketing

Aligning your reward programs to the individualized needs of each consumer should also go beyond simple demographics. The ability to personalize how you market your card reward programs grows exponentially as you leverage your cardholders’ existing transaction behaviors. Using tools such as Predictive Analytics from Raddon can help you identify and even anticipate the needs and wants of individual cardholders, and then personalize the marketing messages accordingly.

After gaining a better understanding of the types of rewards each cardholder wants, you can then begin to structure and tailor specific rewards that are more likely to encourage usage. An example of this would be increasing cashback or reward points for specific spending categories that might resonate with an individual. Also consider mobile-exclusive bonuses (additional points or cashback for transactions made through mobile wallets) and sign-up bonuses, such as an immediate $10 statement credit when a cardholder designates your card as their primary mobile-payment method.

3. Enhance the digital experience

A seamless digital experience is of course critical for mobile-first consumers. Focus on frictionless card provisioning that makes it easy for consumers to add their card to Apple Pay, Google Pay, or Samsung Pay with a one-tap option within your mobile banking app. Being able to provide instant digital card issuance can also help prevent disruption in mobile payments in the case of fraud or lost cards. Delivering real-time spending insights in the form of push notifications and categorized spending reports can also add value and enhance the digital experience beyond just transactions.

Also, be on the lookout for opportunities to improve the digital experience via in-person interactions. An example of this would be reviewing your onboarding process when a new credit or debit card is opened in person at a branch. This is an opportunity to have your branch personnel walk the customer through adding the card not only to the mobile wallet, but also all of the ancillary apps where a consumer may be storing card credentials (such as Uber, Netflix, Amazon, Starbucks, etc.).

4. Optimize security and trust

In our recent nationwide survey of consumers, one-half (49%) experienced fraudulent activity that impacted their financial accounts. With consumers on heightened alert for fraud and becoming more likely to prioritize security in their payment choices, card issuers should highlight the fraud protection benefits they offer. Real-time fraud alerts, biometric and multifactor authentication for your app or simply reminding your cardholders that they are protected against unauthorized transactions can all help to provide reassurance that you offer best-in-class fraud protection.

From loaded to preferred, the ultimate goal

As mobile payments become the default transaction method, financial institutions must proactively position their card as the primary option within digital wallets. The battle for top-of-wallet status isn’t just about loading a card, it’s about ensuring consumers choose it for their everyday spending. By offering strong incentives, seamless digital experiences, security assurances and personalized engagement, financial institutions can increase their share of mobile payments and solidify their position in the digital financial landscape.

In a world where 90% of mobile-wallet users default to one card, ensuring that card is yours is more critical than ever.

Want to ask us a question?

Interested in our services?

We’re here to help.

![]()

![]()

2900 Westside Parkway

Alpharetta, GA 30004

© 2025 Fiserv, Inc., or its affiliates.